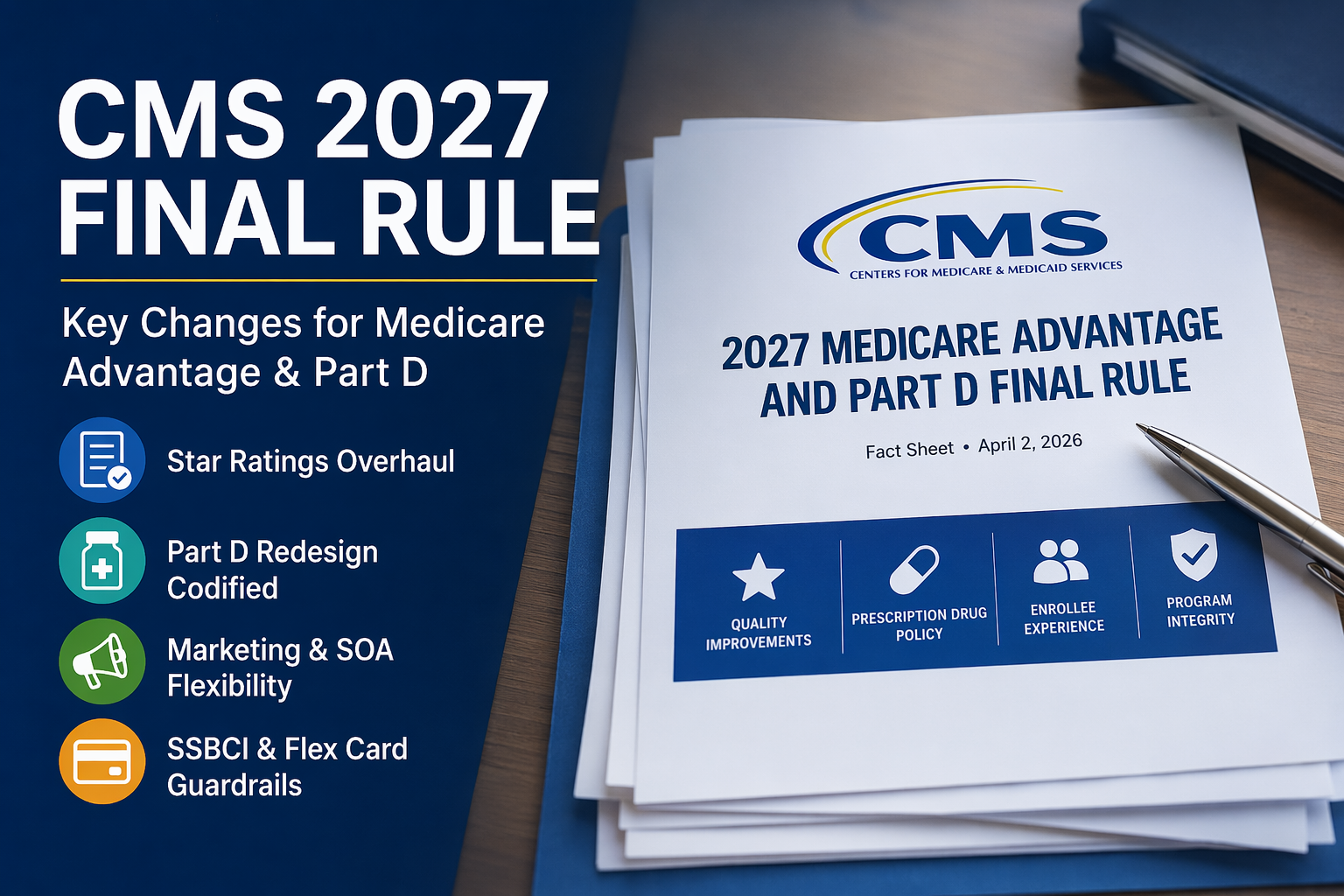

CMS’s 2027 Medicare Advantage and Part D Final Rule: What Changed, Why It Matters, and What It Means for Beneficiaries, Brokers, and the Medicare Market

On April 2, 2026, CMS released its Contract Year 2027 Medicare Advantage and Part D Final Rule, one of the most meaningful Medicare regulatory updates in recent years. While some annual rules feel technical and distant, this one reaches directly into the day-to-day Medicare experience: how beneficiaries compare plans, how agents communicate, how prescription drug costs work, how supplemental benefits are structured, and how health plans will be measured going forward. The rule was published in the Federal Register on April 6, 2026, becomes effective June 1, 2026, and many of the marketing-related changes take effect for the 2027 selling season beginning October 1, 2026.

At a high level, CMS is sending a clear message. The agency wants less regulatory clutter around administrative mechanics, more focus on clinical outcomes and patient experience, more structure around supplemental benefits that have grown rapidly in recent years, and permanent rules for the Inflation Reduction Act’s Part D redesign. In other words, this is not just a cleanup rule. It is a directional rule. It shows where Medicare Advantage and Part D are heading next.

1) CMS is reshaping Star Ratings around outcomes, not paperwork

One of the biggest pieces of the final rule is CMS’s overhaul of the Star Ratings system. CMS says it is refocusing the measure set on clinical care, outcomes, and patient experience by removing measures it sees as administrative, overly topped-out, or no longer useful in helping beneficiaries distinguish one plan from another. For 2027 Stars, CMS is also declining to implement the Excellent Health Outcomes for All reward and will continue the historical reward factor instead. CMS is further adding a new Part C Depression Screening and Follow-Up measure for the 2027 measurement year, which will affect the 2029 Star Ratings.

This matters because Stars are not just a consumer comparison tool. They also drive Quality Bonus Payments and affect plan rebates. So when CMS removes 11 measures and changes the reward structure, it is not a cosmetic adjustment. It changes what plans prioritize, what they invest in, and how they compete. Bass, Berry & Sims noted that the shift away from the Health Equity Index reward and back to the historical reward factor favors consistently high performance across all enrollees rather than a narrower reward tied to a subset of members. RISE went further, noting that CMS estimated the Star changes could produce substantial additional quality bonus payments over time, while also creating a harder environment for some SNP-focused contracts.

For beneficiaries, the pitch from CMS is simplicity: better apples-to-apples comparison. For plans, the reality is more strategic. The era of accumulating Stars through process-heavy administrative optimization appears to be narrowing. The bar is moving more toward measurable results.

2) The IRA-driven Part D redesign is no longer a temporary transition, it is now baked into regulation

Another major section of the rule permanently codifies the Medicare Part D redesign created by the Inflation Reduction Act of 2022. Through 2026, CMS had been implementing those changes through program instructions. Now CMS is putting the framework directly into regulation for 2027 and beyond. That includes eliminating the old coverage gap phase, maintaining a lower annual out-of-pocket structure, eliminating enrollee cost-sharing in the catastrophic phase, and formally incorporating the Manufacturer Discount Program that replaced the old coverage gap discount program. CMS also codified related technical rules involving TrOOP calculations, specialty-tier rules, reinsurance methodology, and the Selected Drug Subsidy.

This is a huge deal because it turns what had felt like a fast-moving implementation phase into a more durable operating reality. The donut-hole era is effectively over as the dominant consumer story. The new consumer story is simpler: drug spending has a clearer ceiling, catastrophic cost sharing is gone, and the financing structure behind Part D has been redesigned in a more formal way. Industry articles from Senior Market Sales, Quotit, Spark, and Ritter all highlighted this codification as one of the biggest stabilizing features of the rule.

For brokers and agencies, this means Part D conversations matter more, not less. Simpler benefit phases do not eliminate confusion. They shift confusion. The challenge now is helping members understand what counts toward their out-of-pocket exposure, how plan design can still vary, and why the “cap” is not always as simple in practice as the headlines make it sound.

3) CMS just made the sales workflow much more flexible for agents and TPMOs

If there is one section of the final rule that agents and agencies reacted to immediately, it is the rollback of several marketing timing restrictions. CMS finalized elimination of the 48-hour waiting period between completion of a Scope of Appointment and a personal marketing appointment. CMS also finalized elimination of the 12-hour gap between an educational event and a marketing event held in the same location, and it now allows SOA forms to be collected at educational events. CMS’s reasoning is that these timing rules created access barriers and operational friction without delivering a measurable enough beneficiary protection benefit to justify the burden.

That is why so many agency and LinkedIn writeups are calling this the most broker-friendly rule in years. Spark, Quotit, Ritter, Tidewater, and multiple LinkedIn commentators all zeroed in on the same operational reality: same-day appointments become easier, warm leads are less likely to die in a forced delay window, educational events become more useful, and scheduling becomes more natural.

Still, this should not be misunderstood as a free-for-all. The SOA itself remains required. Educational events still need to remain educational. CMS did not remove the obligation for plans, agents, and TPMOs to avoid misleading marketing or to document properly. What changed is the timing friction, not the underlying compliance standard.

4) TPMO disclaimers are changing, and that will matter in the real world

The final rule also updates TPMO disclaimer requirements. Based on the Federal Register discussion and the way multiple industry sources summarized the rule, the practical takeaway is that disclaimers are still required, but CMS relaxed when and how they need to appear in some contexts, including removing the SHIP reference from the standard disclaimer language in favor of 1-800-MEDICARE. Several broker-facing summaries also emphasize that the disclaimer no longer has to come within the first 60 seconds of a call, though it still must be delivered before moving into certain plan-benefit discussions.

This looks small on paper, but it matters in real conversations. One of the biggest complaints from agents has been that highly scripted openings can feel awkward, robotic, and distrust-building rather than trust-building. CMS seems to be acknowledging that compliance language should not unnecessarily distort the start of an interaction if the beneficiary can still be properly informed before specific benefits are discussed.

At the same time, consumer advocates are wary. Georgetown’s Medicare Policy Initiative argued that this final rule reflects a broader deregulatory push that rolls back several recent marketing protections. That does not mean CMS is abandoning oversight, but it does mean the burden shifts more heavily onto plans, agencies, and brokers to prove that simplification is not being used as cover for more aggressive sales behavior.

5) CMS tightened the rules around SSBCI, flex cards, and supplemental benefit administration

One of the most overlooked sections of the final rule may end up being one of the most important. CMS finalized two major supplemental-benefit policies: stronger SSBCI administration rules and clarified requirements for debit-card-based supplemental benefits. Plans will have to publicly post their SSBCI eligibility criteria, and debit cards must be electronically linked to covered items and services using a real-time identification method at the point of sale. CMS also made clear that debit cards must be limited to the specific plan year.

CMS also clarified that cannabis products illegal under applicable state or federal law are not allowable as SSBCI. That matters because supplemental benefits have exploded as a marketing theme in recent years, especially with flex cards, grocery-style benefits, and broad value-based add-ons. CMS is not shutting those benefits down. It is drawing harder lines around how they must be structured, verified, and explained.

This is a major signal to the market. If the first chapter of modern supplemental benefits was expansion, the next chapter may be standardization and auditability. Plans that used debit cards because they looked consumer-friendly now have to make sure those tools are operationally defensible as well.

6) Not everything proposed made it into the final rule

That is important. Several industry summaries stressed that you cannot understand the final rule only by looking at what changed; you also have to look at what CMS declined to finalize. The clearest example is the proposal to create a special enrollment period for provider terminations, which CMS explicitly said it is not finalizing in this rule. CMS said it recognizes strong stakeholder interest and may consider future rulemaking in the area.

Quotit also highlighted that the proposal to ban marketing the dollar value of supplemental benefits was not finalized. That matters because it preserves room for plans and marketers to continue emphasizing supplemental-value narratives, at least for now, even while CMS is tightening the operational structure underneath some of those benefits.

For agencies and brokers, this is a reminder not to overread the rule. CMS moved aggressively in some places and held back in others. The direction is not purely deregulatory or purely restrictive. It is more selective than that.

7) So what is CMS really doing here?

The fairest reading is that CMS is trying to do three things at once.

First, it is trying to simplify the beneficiary and broker experience by removing rules that many stakeholders considered unnecessarily rigid, especially around appointment timing and event sequencing.

Second, it is trying to move quality policy away from administrative check-the-box metrics and back toward clinical outcomes, experience, and visible performance differentiation.

Third, it is trying to put more guardrails around areas of Medicare Advantage that have become harder to govern consistently, especially supplemental benefits and their real-world execution.

That combination is why the rule has triggered such mixed reactions. Broker organizations and agencies see badly needed relief. Consumer-protection voices see meaningful rollback risk. Health plans see both opportunity and pressure. And beneficiaries will likely feel the effects first through easier plan conversations, changing Star dynamics, and more standardized Part D rules.

8) What agencies, brokers, and Medicare organizations should be doing now

The timeline matters. The rule is effective June 1, 2026, and CMS says the marketing and communications provisions apply beginning October 1, 2026. That means organizations do not have the luxury of waiting until late AEP prep. Agencies should already be reviewing SOA workflows, educational-event protocols, call scripts, disclaimer language, call-retention processes, and training materials.

For plans, this is also the time to stress-test how flex-card and SSBCI programs are being described, adjudicated, and documented. Publicly posted eligibility criteria and real-time verification expectations mean operational sloppiness will be harder to hide.

For beneficiaries, the ideal outcome is straightforward: easier access to information, simpler drug-cost design, more meaningful plan comparisons, and fewer confusing benefit gimmicks. Whether the market actually delivers that result will depend less on the final rule itself and more on how responsibly stakeholders use the flexibility CMS just gave them.

Final thought

The 2027 CMS Final Rule is not just another annual Medicare update. It is a reset. It eases some of the friction that agencies, brokers, and TPMOs have been fighting for, but it also tells the industry that the future will demand cleaner execution, clearer benefit structures, and more meaningful quality performance. The organizations that win under this rule will not be the ones that simply move faster. They will be the ones that use that added flexibility to become more transparent, more organized, and more member-focused than the market around them.

Your Next Level Starts Here

Ready To Grow Your Medicare Business The Right Way?

Join Advantage Plus and plug into a system built for serious Medicare agents. Get access to top-tier contracts, daily training, real compliance support, and a platform designed to help you grow your book the right way without giving up control of your business.

Book a Demo